Since April 2022, the SMM rebar production schedule sample has been expanded to include 56 enterprises.

According to the SMM survey data from 56 key steel-producing enterprises:

- The planned rebar production for May was 9.3153 million mt, an increase of 360,500 mt from the actual production in April, representing a growth of 4.03%;

- The planned wire rod production for May was 3.6894 million mt, an increase of 185,700 mt from the actual production in April, representing a growth of 5.30%.

Chart-1: Rebar & Wire Rod Production Schedule of Mainstream Construction Steel Mills (56 Enterprises)

Source: SMM

By region (56 enterprises):

North-east China: The total planned rebar production was 370,000 mt, unchanged MoM. The total planned wire rod production was 100,000 mt, unchanged MoM;

North China: The total planned rebar production was 1.31 million mt, an increase of 98,000 mt MoM, representing a growth of 8.09%. The total planned wire rod production was 655,000 mt, an increase of 84,000 mt MoM, representing a growth of 14.71% MoM;

East China: The total planned rebar production was 4.7353 million mt, an increase of 297,300 mt MoM, representing a growth of 6.7%. The total planned wire rod production was 2.0554 million mt, an increase of 136,400 mt MoM, representing a growth of 7.11% MoM;

Central-south China: The total planned rebar production was 1.194 million mt, an increase of 12,000 mt MoM, representing a growth of 1.02%. The total planned wire rod production was 290,000 mt, a decrease of 63,000 mt MoM, representing a decline of 17.85% MoM;

North-west China: The total planned rebar production was 817,000 mt, a decrease of 83,000 mt MoM, representing a decline of 9.22% MoM. The total planned wire rod production was 203,000 mt, an increase of 8,000 mt MoM, representing a growth of 4.10% MoM;

South-west China: The total planned rebar production was 889,000 mt, an increase of 36,200 mt MoM, representing a growth of 4.24% MoM. The total planned wire rod production was 386,000 mt, an increase of 20,300 mt MoM, representing a growth of 5.55% MoM.

Chart-2: Monthly Rebar Production Changes by Region

Source: SMM

Chart-3: Monthly Wire Rod Production Changes by Region

Source: SMM

Overall:

In April, the national construction steel prices first declined and then rebounded. In the early part of the month, the tariff hikes overseas affected the overall trend of bulk commodities. In the mid-to-late part of the month, after the market panic subsided, coupled with frequent rumors of crude steel production restrictions and the release of stockpiling demand ahead of the Labour Day holiday, the market performance improved significantly. On the cost side, the raw material prices in April generally followed a similar trend to finished steel prices, with relatively small fluctuations in steel mill profits. The overall profitability remained within the range of (-200-200). In the east and north China regions, some steel mills reduced their production of rolled steel and increased their production of construction steel. Additionally, some steel mills resumed production after maintenance, leading to a significant increase in production. However, in the central and north-west China regions, the profitability was lower than that in coastal areas. Some manufacturers arranged maintenance plans and diverted part of their pig iron to wide and heavy plate lines, slightly affecting the production of construction steel.Several steel mills are facing a shortage of wire rod specifications. To replenish market resources, there was a slight preference for pig iron to be allocated to wire rod production in May, resulting in a slightly greater increase in wire rod production compared to rebar.

By region:

In north-east and south-west China, steel mill profits ranged from (-100 to 100) yuan/mt. Currently, production efficiency is hovering around the break-even point, with steel mills generally maintaining their previous production levels, showing relatively small overall changes.

In north China, steel mill profits ranged from (-200 to 200) yuan/mt. There is a significant divergence in profits among steel mills in the region, with some manufacturers incurring losses of nearly 200 yuan/mt. Therefore, there are plans for blast furnace maintenance in May, leading to a corresponding reduction in building materials production. However, other manufacturers are experiencing relatively good overall profitability and plan to reduce sheet production and increase rebar and wire rod production in May. Additionally, some steel mills previously produced a small volume of coiled rebar, leading to a shortage of specifications at construction sites. In May, they will increase coiled rebar production, primarily to replenish specifications.

In east China, steel mill profits ranged from (0 to 200) yuan/mt. Steel mills in the region are experiencing good profitability in producing building materials, with significant increases in rebar and wire rod production. Some manufacturers have plans for sheet rolling line maintenance in May, which will redirect surplus pig iron to building materials production. Secondly, some steel mills have resumed blast furnace production, leading to a corresponding increase in the production of various product categories. The overall production changes of multiple steel mills in the Jiangsu region are relatively small, mainly because some manufacturers had a high volume of billet sales orders in late April and are temporarily continuing their previous production plans.

In north-west China, steel mill profits ranged from (-200 to 100) yuan/mt. Currently, some steel mills are generating positive cash flow from building materials production but are still incurring net losses. To replenish some coiled rebar specifications, there is a slight shift from rebar to coiled rebar production. Additionally, steel mills in the region have plans for bar and wire rod maintenance in mid-to-late May, leading to a significant decrease in overall rebar production.

In central and south China, steel mill profits ranged from (-100 to 100) yuan/mt. Some steel mills in the region have extended blast furnace maintenance until mid-to-late May, resulting in a continued decrease in building materials production. Additionally, some steel mills have received a good volume of orders for wide and heavy plates, causing pig iron to be redirected to sheet production.

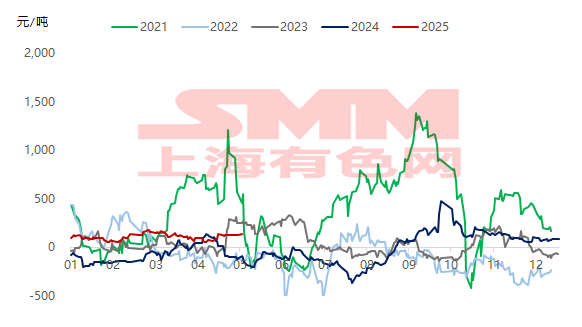

Chart-4: Trend of real-time profits for rebar production by steel mills from 2020 to present

Data source: SMM

Chart-5: Marginal profit situation for rebar production at sample steel mills in early May

Data source: SMM

Looking ahead, the profit performance of blast furnace steel mills this year is expected to be stronger than that of the same period last year, with steel mills in the coastal regions of east China leading in profitability. Although some manufacturers have a high volume of billet sales orders, other manufacturers, due to their relatively good profitability, are expected to redirect pig iron to building materials production after blast furnace resumptions or reduce sheet production and increase rebar production. This is expected to lead to a certain increase in overall building materials production by steel mills in May. However, the profitability of short-process steel mills has remained relatively poor throughout the year. Some regions are facing difficulties in sourcing cost-effective steel scrap, and spot prices are continuing to hover at low levels, making it difficult for profit margins to improve. In the short term, some electric furnace mills are planning to reduce operating hours or suspend production, and production is expected to continue at a medium-to-low level in the later period.Demand side, the number of rainy days increased in south China in May, slightly restricting construction at downstream sites. Additionally, the wheat harvest season in northern China from late May to early June will likely lead to a deterioration in demand in the later period. Overall, steel mill production is currently profit-driven. With blast furnace steel mills generally generating cash flow profits, the momentum for producing construction materials remains strong. However, as demand gradually transitions into the off-season, an increase in supply and a decrease in demand are not conducive to the strengthening of spot prices. It is expected that the spot trend of construction steel in May will likely be in the doldrums.

![The most-traded BC copper contract closed down 2.85%, as speculative fervor cooled, weighing on copper prices [SMM BC Copper Review]](https://imgqn.smm.cn/usercenter/CYktX20251217171711.jpg)

![The Black Industrial Chain Lacked Upward or Downward Momentum Before the Holiday [SMM Steel Industry Chain Weekly Report]](https://imgqn.smm.cn/usercenter/FRcmT20251217171746.jpg)

![The most-traded SHFE tin contract plummeted more than 8% in a single day, and tin prices are expected to remain in the doldrums in the short term [SMM Tin Futures Review]](https://imgqn.smm.cn/usercenter/LLUUJ20251217171751.jpeg)